Thế nhưng Nga vừa xính vính thì các con giời Mỹ cũng tan hoang. Ngành “dầu đá phiến” vừa ngoi lên đã lăn đùng ra dãy đành đặch.. sa thảo công nhân, tài chính rút vốn v.v

Thị trường tiêu thụ cũng KHÔNG MUA DÀU theo “công thức chính qui” : lượng mua tăng khi “đại hạ giá”!. Giá dầu cứ xuông và người sản xuất tiêu thụ chẳng thèm mua, trong khi giá xăng thành phẩm nhiên liệu cho giao thông căn bản của đại khối quần chúng chẳng thèm rẻ xuống đúng mức cho dân nhờ, khi lương bổng trì trệ và lạm phát gia tăng!

Tầu là nước NHẬP DẦU NHIỀU NHẤT THẾ GIỚI từ sau khi mở cửa và nhận chuyển giao công nghệ từ Âu Mỹ, dù có sản xuất dầu hỏa, nhưng không xuất cảng…cũng NGƯNG MUA DẦU VÀO CHO KHO TRỮ…

Người ta dân chúng vốn nọa tính tư duy, cứ nghe mua bán tồn trữ v.v là nghĩ đơn giản như gia dình mua bán nhiều khi có dại hạ giá (on sale). Còn bọn khoa bảng và chuyên gia thì tối dạ chỉ nắm mắt nói theo sách vở vốn toàn giảo thuyết bịp bợm, nhưng hung hăng dự đoán và sai tùm lum…

Luu trữ dầu hỏa là cả một vấn đề. Nó bốc hơi và nguy hiểm. Cần cả một mặt bằng lẫn kỹ thuật cao cấp và an ninh để lưu kho..Nói gọn, tốn phí lắm lắm chứ không phải chơi! Nhưng đặc biệt quan trọng có một nguyên nhân mà các con giời “chuyên da” không hô hoán… đó là khi tiêu thụ đình trệ, thì sản xuất cũng phải giảm sút. Sản xuất giảm sút , nghĩa là nhu cầu DẦU HỎA cũng tụt dốc. Và khi nhu cầu dầu hỏa tụt dốc thì đương nhiên giá dầu không thể ĐỨNG VỮNG, huống hồ gì có mấy “thằng đàn anh” cố tình BÁN RẺ vì mục tiêu “chính trị riêng tư”, thì nó xuống nằm ì ra đó là phải rồi! Vấn đề là nhà nước chúng nó chẳng coi sinh mạng hạnh phúc của dân chúng ra cái đinh gì hết, mà người dâm cứ nhắm mắt tin vào các “lãnh đạo” và “chuyên gia”: mới đáng nói.

Nhà nước chính phủ, chúng nó xem dân như những con cờ đồ vật.. Nhưng dân lại kính ngưỡng nhà nước như thần thánh, cha mẹ! Chúng nó hành dân, tạo khủng hoảng, bắt đi chết trong các cuộc chiến tranh… Rồi “đổi mới”, rồi “xin lỗi”, rồi “điều chình”… thế là dân chổng mông vái tạ hàm ơn.. không nhớ và chẳng biết rằng cái khốn nạn vừa qua chính là do thằng nhà nước chính phủ nó tạo ra! Nó là thủ phạm chứ chẳng phải “anh hùng”…

Nhìn dân Hy lạp mà ngao ngán! Đến mức hiển nhiên như thế mà dân cứ để cả lũ chính trị gia bịp.. Vẫn không dám bước ra khỏi cái ma trận Liên Âu và đồng tiền thổ tả Euro dụng cụ nô lệ! Nhưng cứ đòi giải quyết vấn đề “kinh tế quốc gia”, một cách đòi lược từ nhà sư!!! Hay thẳng thắn hơn, đòi hành xử lương thiện trong “thị trường”. VI NHÂN BẤT PHÚ, VI PHÚ BẤT NHÂN.

Nhân Chù.

21-03-2015

====

Just as Global Oil Glut Deepens, China Cuts Oil Imports

“We don’t want to lose our share in the market,” Kuwait Oil Minister Ali al-Omair said on Thursday. OPEC had to maintain production despite the plunge in price since last summer, he said, underscoring Saudi Arabia’s position. OPEC would not cut production to goose prices. It would not let the American fracking boom off the hook.

The price of oil promptly dropped, annihilating much of the Fed-inspired rally the day before.

No one wants to cut production. In the US, production is still soaring. Demand is lackluster. What gives? Crude oil is piling up around the globe.

Commercial inventories across all OECD countries can now supply 28 days’ of OECD demand, near the very top of the range, the EIA reported.

In the US, the amount of oil in commercial storage facilities (not counting the Strategic Petroleum Reserve) is at historic highs. Another 9.6 million barrels were added during the latest week. To put that in perspective: the US produces 9.3 million barrels per day. So in one week, the US added nearly one day’s production to its already high crude oil stocks! According to the EIA, stocks now amount to 458.5 million barrels, up 22% from a year ago.

By another measure, at the end of February the US was sitting on 29 days’ supply, the most since the 1980s when the last big oil bust was wreaking havoc in the American oil patch.

Speculation is now running wild that the US will run out of crude oil storage capacity. Some voices are claiming that storage in Cushing, Oklahoma, which accounts for 14% of the US total and serves as delivery point for WTI futures contracts, could be full by April.

These speculations have dollar signs at the other end. When storage gets scarcer, or when the perception can be stirred up that it will get scarcer, storage fees jump, boosting revenues and profits of the storage companies. There’s money to be made, as long as the speculation can be maintained. And so the insiders came out all guns blazing.

“Demand for our storage services in Cushing has been robust,” said Robb Barnes, senior VP for commercial crude oil at Magellan Midstream Partners LP, according to Bloomberg. The company has 12 million barrels of storage capacity in Cushing, and all its tanks had been leased, it said.

Fees have been rising “fairly rapidly over the last six months,” Blueknight Energy Partners CEO Mark Hurley told investors. The company has 6.6 million barrels of capacity at Cushing.

All publicly traded storage companies have told investors that profits in 2015 would be higher than in 2014. At least someone is making money during the oil bust.

And it’s not just in the US.

“You’ll find all the locations around the world that can store crude now, like Saldanha Bay or the Caribbean, are going to be full,” said Jared Pearl, commercial director of VTTI in Rotterdam. The group includes Vitol, the largest independent oil trader. “It would be crazy if they weren’t.”

And just when we might be tempted to think – cynical as we are about these sorts of things – that they were just talking their book, China, second largest oil consumer in the world, chimes in.

China has been buying cheap oil since August to fill its Strategic Petroleum Reserves. This buying has been one of the demand drivers in Asia and has provided some support even while prices crashed. The government keeps largely mum about the SPR. But the plan is to increase it to around 600 million barrels, which would be about 90 days’ worth of imports. According to Reuters, most estimates place current storage levels at 30-40 days’ worth of imports. In December, China imported an all-time record of 7.2 million barrels per day. Alas…

“I don’t think there is much space left to fill,” a Chinese storage executive told Reuters under the condition of anonymity. He said that in the Zhoushan area of Zhejiang province, where two SPR bases and major commercial storage facilities are located, tanks “are so full that one VLCC tanker owned by a state refiner has had to wait for almost 15 days to discharge.”

Then there is the demand issue. The Chinese economy is growing, according to government figures, at the slowest rate in 25 years. And now there are expectations that refiners could process less crude in the second quarter. So China will likely curtail its purchases, at least temporarily.

Including China, Asian crude oil imports overall have dropped 5% from the peak in December, according to Thomson Reuters data. Imports by India were down 20% in February from a year ago; imports by Japan were down 11%, largely due to the approaching refinery maintenance season.

Even if these folks are talking their book to goose storage fees, one thing is clear: storage levels are high around the globe, and they’re still rising, while demand is nothing to write home about. It adds to the picture of a worsening global oil glut that will continue to pressure prices, bloody up producers, and maul investors and lenders.

The fracking boom in the US started with natural gas. And now it’s destroying its investors. Read… Investors Crushed as US Natural Gas Drillers Blow Up ====

Investors Crushed as US Natural Gas Drillers Blow Up

by Wolf Richter • March 18, 2015

The Fed speaks, the dollar crashes. The dollar was ripe. The entire world had been bullish on it. Down nearly 3% against the euro, before recovering some. The biggest drop since March 2009. Everything else jumped. Stocks, Treasuries, gold, even oil.West Texas Intermediate had been experiencing its biggest weekly plunge since January, trading at just above $42 a barrel, a new low in the current oil bust. When the Fed released its magic words, WTI soared to $45.34 a barrel before re-sagging some. Even natural gas rose 1.8%. Energy related bonds had been drowning in red ink; they too rose when oil roared higher. It was one heck of a party.

But it was too late for some players mired in the oil and gas bust where the series of Chapter 11 bankruptcy filings continues. Next in line was Quicksilver Resources.

It had focused on producing natural gas. Natural gas was where the fracking boom got started. Fracking has a special characteristic. After a well is fracked, it produces a terrific surge of hydrocarbons during first few months, and particularly on the first day. Many drillers used the first-day production numbers, which some of them enhanced in various ways, in their investor materials. Investors drooled and threw more money at these companies that then drilled this money into the ground.

But the impressive initial production soon declines sharply. Two years later, only a fraction is coming out of the ground. So these companies had to drill more just to cover up the decline rates, and in order to drill more, they needed to borrow more money, and it triggered a junk-rated energy boom on Wall Street.

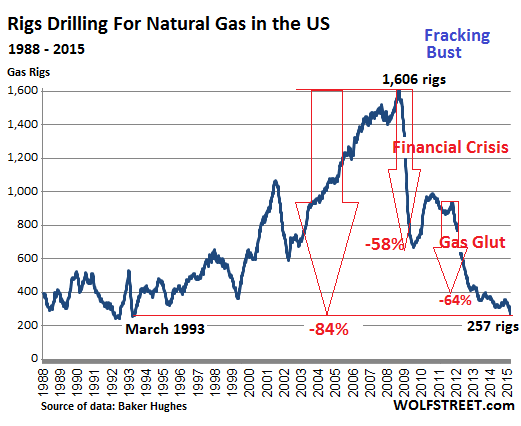

At the time, the price of natural gas was soaring. It hit $13 per million Btu at the Henry Hub in June 2008. About 1,600 rigs were drilling for gas. It was the game in town. And Wall Street firms were greasing it with other people’s money. Production soared. And the US became the largest gas producer in the world.

But then the price began to plunge. It recovered a little after the Financial Crisis but re-plunged during the gas “glut.” By April 2012, natural gas had crashed 85% from June 2008, to $1.92/mmBtu. With the exception of a few short periods, it has remained below $4/mmBtu – trading at $2.91/mmBtu today.

Throughout, gas drillers had to go back to Wall Street to borrow more money to feed the fracking orgy. They were cash-flow negative. They lost money on wells that produced mostly dry gas. Yet they kept up the charade. They aced investor presentations with fancy charts. They raved about new technologies that were performing miracles and bringing down costs. The theme was that they would make their investors rich at these gas prices.

The saving grace was that oil and natural-gas liquids, which were selling for much higher prices, also occur in many shale plays along with dry gas. So drillers began to emphasize that they were drilling for liquids, not dry gas, and they tried to switch production to liquids-rich plays. In that vein, Quicksilver ventured into the oil-rich Permian Basin in Texas. But it was too little, too late for the amount of borrowed money it had already burned through over the years by fracking for gas below cost.

During the terrible years of 2011 and 2012, drillers began reclassifying gas rigs as rigs drilling for oil. It was a judgement call, since most wells produce both. The gas rig count plummeted further, and the oil rig count skyrocketed by about the same amount. But gas production has continued to rise since, even as the gas rig count has continued to drop. On Friday, the rig count was down to 257 gas rigs, the lowest since March 1993, down 84% from its peak in 2008.

Quicksilver’s bankruptcy is a consequence of this fracking environment. It listed $2.35 billion in debts. That’s what is left from its borrowing binge that covered its negative cash flows. It listed only $1.21 billion in assets. The rest has gone up in smoke.

Its shares are worthless. Stockholders got wiped out. Creditors get to fight over the scraps.

Its leveraged loan was holding up better: the $625 million covenant-lite second-lien term loan traded at 56 cents on the dollar this morning, according to S&P Capital IQ LCD. But its junk bonds have gotten eviscerated over time. Its 9.125% senior notes due 2019 traded at 17.6 cents on the dollar; its 7.125% subordinated notes due 2016 traded at around 2 cents on the dollar.

Among its creditors, according to the Star Telegram: the Wilmington Trust National Association ($361.6 million), Delaware Trust Co. ($332.6 million), US Bank National Association ($312.7 million), and several pipeline companies, including Oasis Pipeline and Energy Transfer Fuel.

Last year, it hired restructuring advisors. On February 17, it announced that it would not make a $13.6 million interest payment on its senior notes and invoked the possibility of filing for Chapter 11. It said it would use its 30-day grace period to haggle with its creditors over the “company’s options.”

Now, those 30 days are up. But there were no other “viable options,” the company said in the statement. Its Canadian subsidiary was not included in the bankruptcy filing; it reached a forbearance agreement with its first lien secured lenders and has some breathing room until June 16.

Quicksilver isn’t alone in its travails. Samson Resources and other natural gas drillers are stuck neck-deep in the same frack mud.

A group of private equity firms, led by KKR, had acquired Samson in 2011 for $7.2 billion. Since then, Samson has lost $3 billion. It too hired restructuring advisors to deal with its $3.75 billion in debt. On March 2, Moody’s downgraded Samson to Caa3, pointing at “chronically low natural gas prices,” “suddenly weaker crude oil prices,” the “stressed liquidity position,” and delays in asset sales. It invoked the possibility of “a debt restructuring” and “a high risk of default.”

But maybe not just yet. The New York Post reported today that, according to sources, a JPMorgan-led group, which holds a $1 billion revolving line of credit, is granting Samson a waiver for an expected covenant breach. This would avert default for the moment. Under the deal, the group will reduce the size of the revolver. Last year, the same JPMorgan-led group had already reduced the credit line from $1.8 billion to $1 billion and had also waived a covenant breach.

By curtailing access to funding, they’re driving Samson deeper into what S&P Capital IQ called the “liquidity death spiral.” According to the New York Post’s sources, in August the company has to make an interest payment to its more junior creditors, “and may run out of money later this year.”

Industry soothsayers claimed vociferously over the years that natural gas drillers can make money at these prices due to new technologies and efficiencies. They said this to attract more money. But Quicksilver along with Samson Resources and others are proof that these drillers had been drilling below the cost of production for years. And they’d been bleeding every step along the way. A business model that lasts only as long as new investors are willing to bail out old investors.

But it was the crash in the price of “liquids” that made investors finally squeamish, and they began to look beyond the hype. In doing so, they’re triggering the very bloodletting amongst each other that ever more new money had delayed for years. Only now, it’s a lot more expensive for them than it would have been three years ago. While the companies – or their assets – will get through it in restructured form, investors get crushed.

And as these investors are pulling back to protect themselves, a special phenomenon occurs. Read… Junk-Rated Oil & Gas Companies in a “Liquidity Death Spiral”

No comments:

Post a Comment